ZeroHedge News

Follow

Wage Growth As A Leading Inflation Indicator

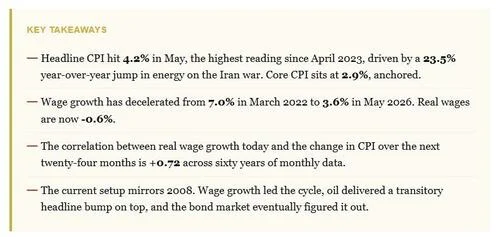

Wage growth, not current inflation, is the key indicator for future price trends. Historically, wage growth has consistently led consumer price index (CPI) peaks. This relationship inverted after 1985 due to factors like Fed credibility and globalization. Prior to 1985, CPI led wages, but since then, wage growth has signaled price pressures months in advance.The current CPI surge is attributed to energy prices, considered temporary noise by the author. Wage growth actually peaked in March 2022 and has been decelerating since. This deceleration in wage growth is leading to negative real wage growth, where prices outpace earnings. Negative real wage growth historically precedes CPI deceleration within 12-24 months.The author draws a parallel not to the 1979 inflation spike, but to the 2008 period. In 2008, an oil shock pushed CPI higher, but underlying real wage compression had already weakened demand. This ultimately led to deflation. The current situation shares structural similarities, with an oil-driven CPI bump on top of decelerating wages.The bearish argument for sustained inflation requires wage growth to re-accelerate and inflation expectations to de-anchor, neither of which is currently supported by data. This suggests that duration in portfolios may be attractive, and equities should favor quality compounders. Inflation is a regime, and the leading indicator, wage growth, points to disinflation. Until wages and expectations change, the focus should remain on wage trends.